The Federal Reserve's policy response to the latest financial crisis can be summed up in one word: unconventional. Between interest on excess reserves (IOER), quantitative easing (QE), and purchases of mortgage backed securities (MBS), the Fed has deployed a wide range of instruments to avoid deflation while preserving financial stability. However, although it is clear the Fed has acted in many ways, what is still unclear is how these policies impact the financial sector and the economy at large. Is interest on excess reserves expansionary or contractionary? Are large scale asset purchases expansionary or contractionary? A rapidly growing and evolving shadow banking sector has only worsened this confusion, and this post is an attempt to make some sense of these arguments in an illustrated form.

First, an introduction to the major players. Interest on Excess Reserves (IOER) originally was a policy implemented by the Federal Reserve in the depths of the financial crisis to expand the Fed's balance sheet to ease liquidity needs. It authorized the Federal Reserve to pay banks interest on their reserves that were in excess of the required amount, and thus gave all commercial banks a risk free return of 0.25% on any extra available cash. However, as a side effect, it meant that banks were unwilling to invest in any security that had a nominal yield of less than 0.25%, as they could just plow that money into excess reserves instead.

IOER was especially important in limiting the inflationary effects of the Fed's Large Scale Asset Purchases. In these programs, the Fed massively expanded its balance sheet by purchasing either long-term treasuries (QEI, QEII), or mortgage backed securities. These purchases have more than tripled the Fed's stock of treasuries from about $480 billion in August of 2008 to $1.64 trillion in August of 2012, raising the monetary base from $884 billion to about $2.61 trillion in the same time period.

These purchases of treasuries have been problematic for the shadow banking sector, notably the oft maligned money market funds, as the purchases have drained the financial system of safe collateral. Money market funds offer a liquid, yet interest bearing fund for large deposits by taking the deposited cash and entering into repurchase agreements, or repos. Repo is a sort of rental arrangement in which the money market fund "rents" out its cash to firms who need liquidity but who do not want to sell their assets. A typical repo involves the money market fund giving another investor cash in exchange for an asset, then after a certain period of time, the investor repurchases the asset and the money market fund gets its cash back with an interest payment. However, the lower the yield on the underlying asset, the smaller the interest rate payment. As a result of the financial crisis' effect on the perceived riskiness of "unsafe" assets, treasuries have become the asset of choice for repos. However, the shortage of safe collateral has pushed down yields on treasuries. As a result, money market funds are surviving on smaller and smaller spreads, putting them in a precarious position and threatening a contraction of collateral chains. The fear is that if this continues, money market funds will collapse and a (shadow) bank run will cause a liquidity and solvency crisis.

This new element of shadow banking makes evaluating monetary policy a headache. Traditionally, expansionary monetary policy in the form of asset purchases works like in the diagram below. When the Fed buys assets, the money that it injects into the market goes to commercial banks who can then lend out the money and make a yield. Also, the market for treasuries doesn't shift that much as banks can also sell their holdings of treasuries, preserving the model of the shadow banks as they can still make some yield off the repo agreement.

However, in the current crisis position, the situation is very different. Because of the safe asset shortage, commercial banks pile into treasuries as a way of getting some yield for their depositors. This is happening at the same time as the central bank buys large stocks of treasuries, thereby contracting the supply of treasuries even further. As a result of high treasury prices, shadow banks struggle as they can no longer provide a sufficient yield. Commercial banks are in a better position than shadow banks because commercial banks can still park their excess reserves at the Fed and earn IOER. They can limit their purchases of treasuries, thus maintaining what is left of the treasury market.

The key question that David Beckworth and Cardiff Garcia are trying to settle is what would removing IOER from the system do? David Beckworth focuses on the money side, and argues that a removal of IOER would be seen as a permanent expansion of the monetary base, thereby rapidly boosting inflation expectations. In response, banks sell off treasuries and invest in riskier assets which keeps shadow banks safe. His world looks much like the following picture:

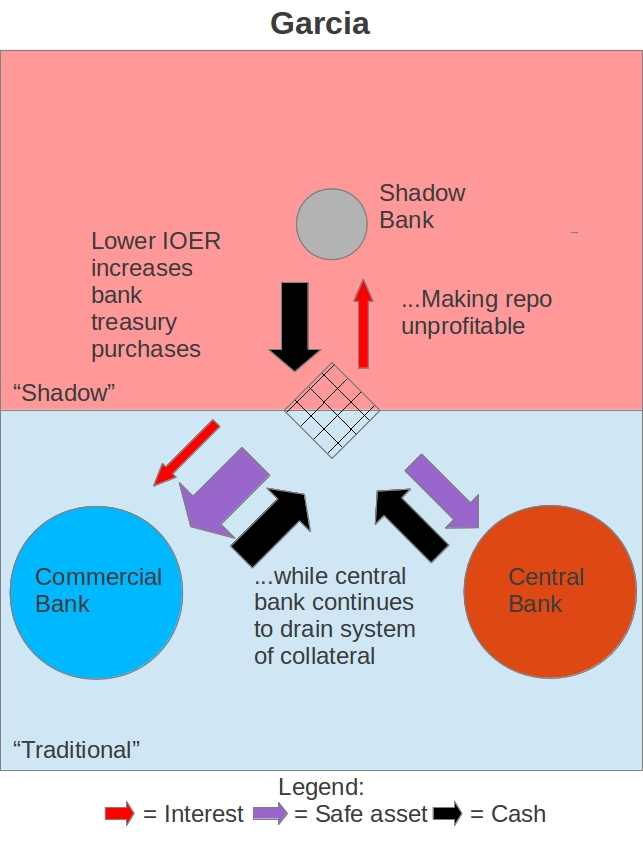

On the other hand, Garcia focuses on credit, and argues that IOER is the only thing keeping treasury interest rates positive. Therefore a removal of IOER would lead to massive expansion of commercial bank purchases of treasuries in search of yield, thereby collapsing the shadow banking sector as the system is drained of safe collateral. His world looks much like the picture below:

The critical difference between the two scenarios is how IOER affects commercial bank purchases of treasuries. Beckworth seems to believe a removal of IOER would push banks into riskier assets, thus causing banks to sell treasuries and keep shadow banks safe. On the other hand, Garcia seems to believe a removal of IOER would not be enough to compensate for the perceived riskiness of non-treasury assets, so banks would purchase treasuries in response to a cut in IOER. This would contract the supply of treasuries, destroying the shadow banking sector.

So which one is correct? To be honest, I don't know for sure, and I'm not sure if either Garcia or Beckworth can be certain about the whole story. But Dan Carrol mentions an interesting option that would perform well in spite of this model uncertainty: sterilized lowering of IOER. In this case, the Fed removes IOER, but then partially compensates for the treasuries bought by commercial banks by selling its own stock of treasuries. The drawing looks something like this:

This might seem counter intuitive as the central bank appears to be doing two actions that seem to contradict each other. Yet if we consider the role of expectations, such a policy becomes much more logical. Given that the monetary base has more than tripled since 2008, it should be clear that the market does not expect that expansion to be permanent. According to Krugman, a fully credible expansion of the monetary base in this period and all future periods should directly lead to inflation. Therefore, since prices have not tripled in response to the change in the base, markets must be pricing in the fact that the base expansion will be sterilized by the Fed in the future.

To raise inflation expectations, the Fed must credibly commit to a future base expansion, and, paradoxically, it cannot do so if the monetary base is too large. Therefore, if sterilized IOER reduction is seen as a move to hitting a nominal target, such as higher NGDP, it can still be part of a credible package that restores the nominal target while preserving the shadow banking sector. In the case of NGDP, a rough estimate of pre-crisis trend growth puts desired NGDP at about $17.3 trillion, about $1.7 trillion dollars above where we are now. Because the average NGDP to Monetary Base ratio over the Great Moderation was about 16.3, a reasonable monetary base would be about $1.06 trillion, $1.59 trillion less than the current monetary base. This means as long as the Fed can credibly commit to permanently expanding the monetary base to around $1.06 trillion, the Fed has room to unwind about $1.59 trillion of treasuries. This would expand the supply of safe collateral and address Garcia's concerns. In addition, giving up on IOER and credibly committing to a permanent base expansion would address Beckworth's call for a regime shift that would restore trend NGDP growth.

A sterilized reduction in IOER would have other advantages as well. First, because its mechanism is not dependent on central bank treasury purchases, there's no risk that shadow banking troubles would lower NGDP growth. Since there's uncertainty about which of Garcia's or Beckworth's scenario would play out, an unsterilized reduction in IOER would translate into uncertainty about whether future NGDP growth should go up or down. Markets would still be uncertain on the status of the shadow banking sector, thus holding back growth.

Second, sterilized cuts in IOER directly commit to a modest increase in the monetary base instead of relying on small monetary frictions. One argument for LSAP's effects on expectations is that an increase in the Fed's balance sheet increases the fraction of its balance sheet expansion that markets expect to be permanent. In other words, the expected future monetary base is convex with respect to the current monetary base. But this approach is fraught with uncertainty and a lack of precision, which may be an issue holding back further monetary easing. If the set of possible inflation rates are {1, 1,2, 1.4, 1.8, 2, 10, 100}, this may change whether the central bank is willing to ease or not. Unwinding the balance sheet while cutting IOER would increase the Fed's precision, improving monetary credibility.

Another framework in which sterilized IOER makes sense is DeLong's law, a modification of Say's law and Walras' law. Say's Law originally said that excess demands for all goods must add up to zero, so there cannot be a general glut.

(equations from Mark Thoma)

However, Walras pointed out that we needed to include money in this model, therefore there can be a general glut in goods if there is excess demand for money. This opens up a role for monetary policy to reduce that excess demand.

DeLong then argues that another factor we need to be aware of in the recent recession is excess demand for safe assets. So Walras' Law should be expanded further:

This framework clearly delineates between what Beckworth, Garcia, and Carrol are proposing. Beckworth argues that lowering IOER directly solves excess demand for money, and therefore goes on to solve excess demand for safe assets. But Garcia argues lowering IOER directly increases excess demand for safe assets to such an extent that it overwhelms any reduction in excess demand for money. So while directly cutting IOER reduces excess demand for money, it's ambiguous whether it reduces the general glut for goods. Carrol's proposal then comes in the middle, as cutting IOER reduces excess demand in money while sterilization reduces excess demand for safe assets.

In the end, this debate shows not only why the market monetarist focus on expectations is important, but also why an analysis of mechanisms cannot be ignored. All of these arguments for sterilized IOER depend on a credible commitment to expand the monetary base, so if the market expects the Fed to maintain a 2% inflation ceiling the policy change would still be useless. However, changing the target without being aware of the collateralized world we live in would also be a failure, as we would be twisting the dials in all the wrong directions, endangering monetary credibility.

So, those currently holding money market funds shift to bank deposits.

ReplyDeleteThose currently borrowing from money market funds shift to borrowing from banks.

The "shadow" banking system collapses.

The regular banking system expands--more deposits and more commercial loans.

Regular banking requires more capital, and so, the interest rates both paid and charged will be higher.

By the way, I don't see much point into this "renting" discusion (other than the notion that credit involves rental arragements for money.) The borrowers from the shadow banking system are borrowing short term using "safe" assets as collateral.

Now, to the degree they do this for cash management purposes, the alternative would be short term borrowing from banks (with collateral perhaps related to their underlying businesses) or else holding larger balances in checkable deposits.

Anyway, the real monetary signicance of all of this is that the interest rate paid on deposits is driven down. And when that becomes more negative than the cost of storing currency, there is a big increase in the demand for currency. The Fed has to accomodate that.

If it weren't for hand to hand currency, the yields on commerical bank deposits could go as negative as necessary to maintain a balance between the quantity of money and the demand to hold it, even if the charges for loans are high and so there is a low quantity of loans demanded and quantity of money.

The "cost" of intermediation is "higher," without the shadow banking system. But given that the shadow banking system always seemed to have a large element of "I can avoid risk by selling out before everyone else," is the lower cost of the shadow banking system just a mispricing of risk?

Since the onset of the Great Recession the Fed has introduced 4 contractionary money policy "tools" (delaying any recovery). But the payment of interest on the member commercial bank's excess reserve balances is the most de-stablizing. Removing this perverted (& Keynsian inspired) policy cannot be accomplished by ignoring monetary policy's principal objective - that policy be formulated in terms of desired rates-of-change (roc’s) in monetary flows (MVt) relative to roc’s in real-gDp.

ReplyDeleteBernanke's policy blunder should be reversed in baby steps. As the member banks reallocate the interbank earning assets held at their respective District Reserve bank, i.e., as IBDD's decrease (the Fed should "wash out" or sterilize these asset conversions) by the approximate volume the non-bank public's holdings of government securities increase.

The payment of interest on excess reserve balances has both: 1. absorbed existing bank deposits within the CB system - acting as a credit control device & 2. attracted monetary savings from the shadow banks (induced dis-intermediation within the non-banks in 2 different ways). IOeR's set up a "collateral squeeze" & reduced the “velocity of pledged collateral”.

“The chains of loaned securities being pledged and re-pledged in the so-called wholesale money markets are growing shorter, as collateral piles up at central banks where it can’t generate additional borrowing.”

IOeR’s alter the construction of a normal yield curve, IOeR’s INVERT the short-end segment of the YIELD CURVE – known as the money market. Excess reserve balances remunerated at .25% are covered by all "close substitutes' extending for up to 2 years under the Daily Treasury Yield Curve's umbrella.

IOeR's result in a cessation of the circuit income & transactions velocity of funds. IOeR's exacerbate stagflation.

Lowering the remuneration rate vis a vis other competitive yielding assets (roa) will result in a shift in the composition of CB earning assets (if CBs are to remain fully invested & are to preserve consistent earnings growth for their owners & stockholders).

ReplyDeleteThe precedent for lowering the remuneration rate on excess reserve balances was set during the 1966 credit crunch. In the administration of its Regulation Q policy the Board allowed the commercial banks during the first seven months of 1966 to pay higher interest rates on certificates of deposit than savings and loan associations and the mutual savings banks could pay on share certificates and savings deposits.

Such an interest rate differential had existed in no other period. It was this factor, unique to 1966, that triggered the residential mortgage credit crisis of that year.

The Board (and the FDIC) reversed their earlier action on July 20, 1966 & made the first reduction in interest rate ceilings on time deposits since February 1, 1935. A second reduction in Regulation Q ceilings was effected on September 26, 1966.

The effects of restoring a rate differential in favor of the intermediaries (analogous to the shadow banking system today where the short-end of the yield curve is inverted) was apparent in the reversal of the trends of the first seven months of 1966. Time deposits in commercial banks which had increased $10.1 billion in the first seven months and stood at a figure of $156.8 at the end of July grew by only $2.0 billion during the remainder of the year.

Share accounts in savings and loan associations by contrast which stood at a figure of $110.9 billion at the end of July had $3.1billion of their total 1966 growth of $3.6 billion during the last five months of the year.

Congress and the Board of Governors should above all pursue a constant flow of monetary savings into real-investment. I.e., the BOG should eliminate the payment of interest on excess reserve balances & remove the FDIC's unlimited guarantee on non-interest bearing transaction accounts (the FDIC should selectively guarantee interest-bearing savings/investment accounts).

There was no need for the Fed's 2 consecutive operation twist programs. The real-rate yield curve would have flattened as soon as the remuneration rate on excess reserve balances was dropped.

The discussion here is a touch off. Cut the .25% in reserve payments, which is in part a back-door way of helping to recapitalize the banks and reduce their risk exposure (that's over $3 billion a year in cash paid to the banks, over four years more than $12 billion), and short term treasury yields will probably go negative. there will still be excess reserves. Treasury prices will be higher. And these lower yields will push money into less-safe assets, lowering those yields. Searching for higher returns, banks will lend out more money.

ReplyDeleteThis all should increase inflation and mean riskier bank balance sheets. It will also mean faster GDP growth.

The only issue the naysayers may have with your proposal to sterilize the IOER reduction is that reverse QE would slow the pace of recovery, while the economy needs to be stimulated. So, on net, your sterilization proposal would not increase the pace of growth, but would just slightly increase banks' risk portfolios.

I agree with previous commented that they should just end IOER and only sterilize it once nominal GDP actually starts to run hot for 2-3 quarters.

banks don't lend reserves!!!!

ReplyDeleteBill, I think the core issue is that MMF's are a key source of liquidity now, so that if we need to resolve the issue it will take time.

ReplyDeleteThornstein, the reason it seems sterilized IOER removal would be better is because if there is a concern about safe asset shortages, increasing collateral in the market would be, on the margin, compensated for by a credible commitment to the future monetary base.

I cannot even pretend to fully comprehend all of what you've written here, but I'm particularly confused by one sentence. You write, "In the case of NGDP, a rough estimate of pre-crisis trend growth puts desired NGDP at about $1.73 trillion, about $1.7 trillion dollars above where we are now." Is this a typo which should be read as "$17.3 trillion" or do I completely misunderstand everything?

ReplyDeleteGood catch. I fixed the typo. Out of curiosity, which parts are not that clear?

ReplyDelete